The Union Budget is a key document which informs the public about the Government’s socio-economic plans and priorities. It is important to critically evaluate this document because of our collective ‘failure to provide for full employment’ and the ‘arbitrary and inequitable distribution of wealth and incomes’; Keynes wrote this in 1936 and it continues to remain the same. Moreover, it is our collective right and responsibility to decide how the government should obtain its revenue and how it must be spent. No formula or algorithm exists for this. As Piketty wrote in his Capital in the Twenty-First Century, ‘Taxation is not a technical matter. It is preeminently a political and philosophical issue, perhaps the most important of all political issues. Without taxes, society has no common destiny, and collective action is impossible.

This blog post aims to outline the priorities of the current central government by examining the expenditure on physical and social infrastructure and the nature of taxes. This is done in 5 charts.

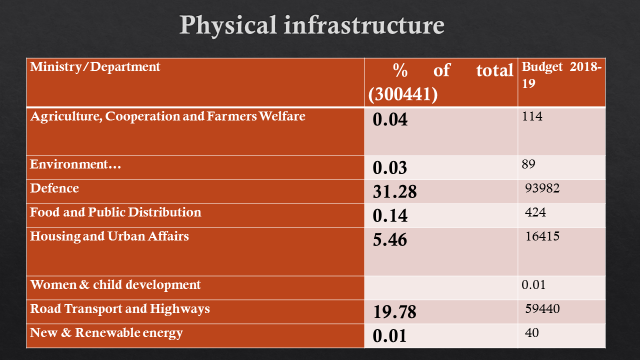

(1) Physical Infrastructure

Defence is significantly more important than roads, housing, food, and farmers’ welfare.

Capital Expenditure of Select Central Ministries (in Rs. Crore)

Source: Expenditure Budget Vol. 1, 2016-17, Statement 2, pp 4-9

All values are rounded off to the nearest crore.

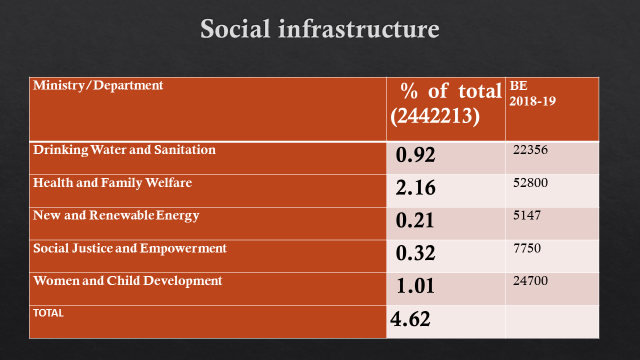

(2) Social Infrastructure

Physical infrastructure creation is more important than social infrastructure creation.

Have the negative effects of physical infrastructure creation been accounted for’

‘Total Allocations of Select Ministries (Rs. 112753 Crore)

Source: BS, p 36, Annex No. III-A to Part A

RE refers to revised estimates which include supplementary demands for funds made by the ministries during the financial year.

BE refers to budget estimates.

(3) Direct & Indirect Taxes

Our taxation policy is regressive due to the high proportion of indirect taxes.

Select Direct and Indirect Taxes (in Rs. Crore)

Source: Receipts Budget, 2018-2019, pp. 2-4

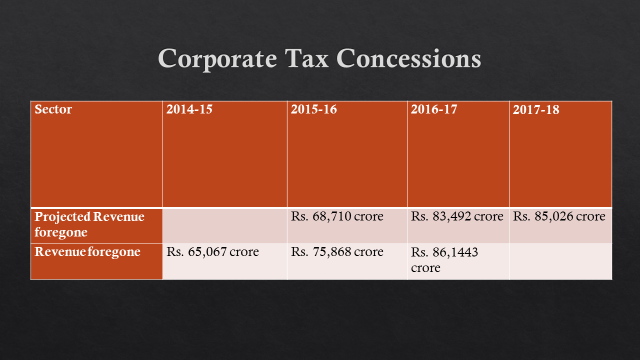

(4) Corporate Tax Concessions

Our tax concessions could approximately fund 75% of the social infrastructure spending estimate.

(5) Corporate Tax Structure

Our corporate taxes are regressive.

Effective tax rate paid by sample companies across range of PBT (FY 2016-17)

Source: Statement of Revenue Impact of Tax Incentives under the Central Tax System: Financial Years 2014-15 and 2015-16, p 30 of the Receipts Budget, 2016-2017, Annex-15.

1 Values rounded off to the nearest integer; hence the total adds up to 101 and not 100. Financial year 2012-13. The number of companies whose PBT is zero is 17,912 and their share in total income is around 9 per cent.

Concluding comments

Our government prioritises defence over agriculture. Our government prioritises physical infrastructure over social infrastructure and does not take into account ecological damage and the displacement caused due to physical infrastructure creation. And our taxation policy is regressive. We must use our collective rights and responsibilities to decide how the government should obtain its revenue and how it must be spent.